The 50/30/20 Rule: The Simplest Budget That Works

Most budgets fail because they’re too complicated. Tracking 47 categories, debating whether coffee is “dining out” or “groceries,” adjusting percentages monthly—it becomes a part-time job. Then life gets busy, and the budget gets abandoned.

The 50/30/20 rule offers a different approach: three numbers, three categories, and enough flexibility to work for almost anyone. It won’t make you a budget ninja overnight, but it will give you a framework that’s actually sustainable.

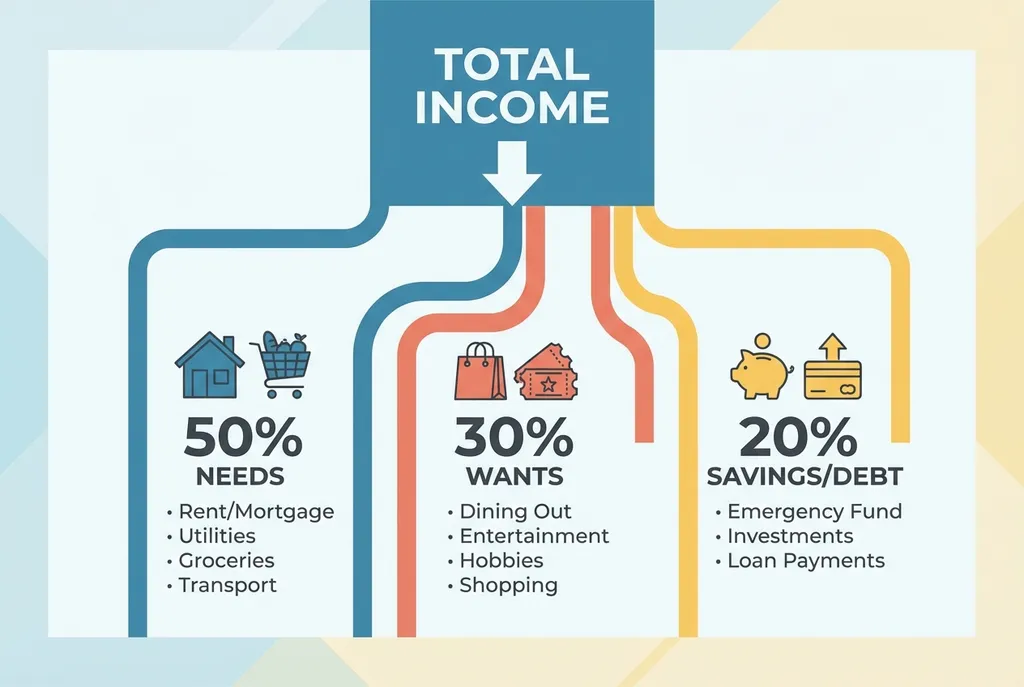

The 50/30/20 Breakdown

Take your after-tax income (what actually hits your bank account). Divide it like this:

| Category | % | What It Covers | Examples |

|---|---|---|---|

| Needs | 50% | Things you must pay to survive and function | Housing, utilities, groceries, transportation, insurance, minimum debt payments, childcare, basic phone/internet |

| Wants | 30% | Things that improve your life but aren’t strictly necessary | Dining out, entertainment, hobbies, gym, nicer-than-necessary versions of needs, shopping, vacations |

| Savings & Debt | 20% | Building your financial future | Emergency fund, retirement contributions, investments, extra debt payments, specific savings goals |

A Real Example

Let’s say your take-home pay is $4,000/month:

| Category | Item | Amount |

|---|---|---|

| Needs (50%) | Rent | $1,200 |

| Utilities | $150 | |

| Groceries | $300 | |

| Car payment + insurance | $250 | |

| Gas | $100 | |

| Subtotal | $2,000 | |

| Wants (30%) | Dining out | $200 |

| Entertainment | $150 | |

| Shopping | $200 | |

| Gym | $50 | |

| Subscriptions | $100 | |

| Hobbies | $150 | |

| Buffer for fun | $350 | |

| Subtotal | $1,200 | |

| Savings (20%) | 401k contribution | $400 |

| Emergency fund | $200 | |

| Extra student loan payment | $200 | |

| Subtotal | $800 |

That’s it. You don’t need a spreadsheet with 50 rows. Three categories, three targets.

Try Your Own Numbers

Adjust your monthly income below to see how the 50/30/20 rule breaks down for your situation:

Why the 50/30/20 Rule Works

It’s Forgiving

Miss your grocery budget by $50? With detailed budgeting, that’s a failure. With 50/30/20, it’s still within your “needs” category—no big deal. The framework absorbs fluctuations without requiring constant adjustments.

It Forces Prioritization

When your needs hit 50%, you’re forced to choose. Is that nicer apartment a need or a want? Is premium car insurance necessary or just comfortable? These questions clarify your priorities.

It Protects Fun

Many budgets make the mistake of cutting all enjoyment. The 30% wants category explicitly protects your quality of life. Sustainable budgets include things you actually enjoy.

It Automates Saving

The 20% isn’t “whatever’s left”—it’s a planned allocation. When you treat savings as non-negotiable (like rent), it actually happens.

It Scales With Income

Whether you make $30,000 or $300,000, the percentages work. The dollar amounts change, but the framework stays constant. This makes it useful across life stages.

The Tricky Part: Defining Needs vs. Wants

Here’s where most people struggle: the line between needs and wants is blurry.

Housing: A roof is a need. But is a $2,500 apartment a need when $1,800 options exist? The extra $700 is technically a want.

Transportation: Getting to work is a need. But is a new car with a $400 payment a need when a used car at $150 works? The upgrade is a want.

Food: Eating is a need. But is organic everything a need? Dining out? A $7 coffee? Mostly wants.

Phone: Communication may be necessary. But is the latest iPhone with unlimited data a need? The baseline plan is a need; the upgrade is a want.

The honest answer: most people undercount their wants by hiding them in the needs category. Be ruthless. If you could survive without it or with a cheaper version, some portion is a want.

What If 50% for Needs Isn’t Possible?

In high-cost cities, housing alone can exceed 50% of income. If you can’t hit the targets, you have options:

Option 1: Increase Income

Side hustles, asking for a raise, switching jobs, developing skills that pay more. The numbers work better with more income.

Option 2: Reduce Needs

Move to a cheaper area, get a roommate, sell the car and use public transit, switch to a cheaper phone plan. These are painful but effective.

Option 3: Accept a Modified Ratio

Maybe your current reality is 60/25/15. That’s okay as a starting point. The goal is to move toward 50/30/20 over time, not achieve it instantly.

Option 4: Adjust the Wants First

If needs are fixed at 55%, maybe wants drop to 25% to protect the 20% savings. Savings is the foundation of financial security—protect it when possible.

Common 50/30/20 Mistakes

Mistake 1: Using Gross Income Instead of Net

The percentages apply to after-tax income—what actually hits your bank account. Using gross income inflates every category and sets unrealistic expectations.

Mistake 2: Hiding Wants in Needs

That premium gym membership isn’t a need. Neither is the upgraded cable package or the newer-than-necessary car. Be honest about what you’re choosing versus what you require.

Mistake 3: Ignoring Irregular Expenses

Car repairs, medical bills, holiday gifts—these hit your needs or wants categories when they occur. Budget for them monthly by setting aside money for irregular expenses.

Mistake 4: Treating It as All-or-Nothing

Missing 50/30/20 by a few percentage points doesn’t mean failure. The framework provides direction. Close counts. Improvement matters more than perfection.

Mistake 5: Not Adjusting for Life Changes

Got a raise? Recalculate. Had a baby? Needs shift. Paid off a debt? Reallocate. The percentages stay constant, but the actual dollars change with life.

The 50/30/20 Rule vs. Other Budgeting Methods

| Method | How It Works | Best For | Complexity |

|---|---|---|---|

| 50/30/20 | Percentage-based categories | Beginners, simplicity seekers | Low |

| Zero-Based | Every dollar assigned | Detail-oriented, control seekers | High |

| Envelope System | Physical cash in categories | Overspenders who need hard limits | Medium |

| Pay Yourself First | Save first, spend the rest | Automation lovers | Low |

| 80/20 Rule | Save 20%, spend 80% freely | Maximum freedom seekers | Very Low |

Choose based on your personality. Need simplicity? Start with 50/30/20. Want more control? Graduate to zero-based.

Making the 50/30/20 Rule Work for You

Calculate Your After-Tax Income

Look at your actual paychecks, not your salary. Include all reliable income sources.

Calculate the Target Amounts

Needs: Income × 0.50. Wants: Income × 0.30. Savings: Income × 0.20.

Track Your Current Spending

Pull 2-3 months of bank statements. Categorize everything into needs, wants, and savings. Be honest.

Compare and Adjust

How does your current spending compare to targets? Where are the gaps?

Make One Change at a Time

Don't overhaul everything at once. Maybe this month you focus on reducing wants by $100. Next month, another adjustment. Small changes stick.

Automate Where Possible

Set up automatic transfers to savings on payday. The 20% happens before you can spend it.

Beyond 50/30/20: When to Graduate

The 50/30/20 rule is training wheels. It teaches the fundamentals:

- Live below your means

- Needs shouldn’t consume everything

- Savings is non-negotiable

- Wants are allowed but limited

Once these concepts are habits, you might want more detailed tracking. Or you might stay with 50/30/20 forever—many financially successful people do.

The “right” budget is the one you actually follow.

Your Action Steps This Week

-

Calculate your actual take-home income for last month. Every dollar that hit your account.

-

Categorize last month’s spending into needs, wants, and savings. Use bank statements. Be ruthless about the needs/wants distinction.

-

Calculate your actual percentages. Were you at 65/30/5? 50/40/10? Knowing where you are is the first step.

-

Identify one adjustment. What’s the easiest change to move closer to 50/30/20?

-

Set up one automatic transfer. Even $50 to savings counts. Automate it to happen right after payday.

The Bottom Line

The 50/30/20 rule divides your income into three simple categories: 50% needs, 30% wants, 20% savings. It’s not perfect, and the percentages may not fit everyone, but it provides a framework that’s actually usable.

Most people don’t need a complex budget. They need a simple guideline that forces two behaviors: keeping needs reasonable and saving consistently.

The 50/30/20 rule does exactly that. Three numbers. Three categories. One sustainable system.

Frequently Asked Questions

What is the 50/30/20 rule?

The 50/30/20 rule divides your after-tax income into three buckets: 50% for needs (rent, utilities, groceries, insurance), 30% for wants (dining out, entertainment, hobbies), and 20% for savings and debt repayment. It's a framework, not a strict requirement.

Who invented the 50/30/20 rule?

Senator Elizabeth Warren and her daughter Amelia Warren Tyagi popularized the rule in their 2005 book 'All Your Worth: The Ultimate Lifetime Money Plan.' They developed it based on decades of bankruptcy research showing that keeping needs under 50% of income is crucial for financial stability.

Is 50/30/20 the same as 50/20/30?

Yes—some sources flip the wants and savings categories, writing it as 50/20/30. The percentages and meanings are identical: 50% needs, 30% wants, 20% savings. The order doesn't matter; the allocation does.

What if I can't fit my needs into 50%?

If needs exceed 50%, you have two options: increase income or reduce needs. High-cost cities often make 50% impossible for housing alone. Consider the rule as a goal to work toward rather than an immediate requirement. Start where you are and gradually shift the percentages.

Does the 50/30/20 rule include debt payments?

Minimum debt payments on necessary debt (mortgage, car loan) count as needs. Extra debt payments beyond minimums count toward the 20% savings/debt category. Credit card debt reduction should come from the 20% since it builds your financial health.

Is 20% savings enough for retirement?

For most people, yes—if started early enough. Someone saving 20% from age 25 will likely have plenty for retirement. Starting later may require higher percentages. The 20% is a solid baseline that works for most situations.

Can I modify the percentages?

Absolutely. The 50/30/20 is a framework, not a law. High earners might do 40/20/40. Those in debt recovery might do 50/20/30 or even 60/10/30. Adjust based on your goals and circumstances while keeping the three-category structure.

Related Articles

Ready to take control of your budget?

Download BUDGT and start tracking your daily spending today.