What is Zero-Based Budgeting? Every Dollar Has a Job

You’ve tried budgeting before. You downloaded an app, set some limits, tracked expenses for a week or two, then life happened. The budget became a vague suggestion rather than a plan. Sound familiar?

Zero-based budgeting is different. It’s not about tracking what you spent after the fact—it’s about deciding what you will spend before the month begins. It’s the difference between recording history and planning the future.

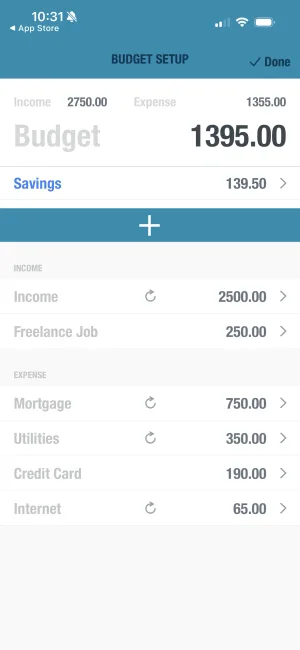

The concept is elegantly simple: your income minus your planned expenses equals exactly zero. Not because you’re broke, but because every single dollar has been assigned a job before you spend it.

The Zero-Based Budgeting Formula

Here’s the math:

Income - Expenses - Savings - Investments = $0

If you earn $4,000 this month, you allocate all $4,000 to specific purposes:

| Category | Amount | % of Income |

|---|---|---|

| Rent | $1,200 | 30% |

| Groceries | $500 | 12.5% |

| Savings | $500 | 12.5% |

| Utilities | $400 | 10% |

| Investments | $400 | 10% |

| Transportation | $300 | 7.5% |

| Misc/buffer | $250 | 6.25% |

| Insurance | $200 | 5% |

| Entertainment | $100 | 2.5% |

| Dining out | $100 | 2.5% |

| Subscriptions | $50 | 1.25% |

| Total allocated | $4,000 | 100% |

| Remaining | $0 |

See It in Action

Adjust your income to see how every dollar gets assigned a purpose:

Every dollar has a job. When remaining equals $0, your zero-based budget is complete.

The zero doesn’t mean you’re living paycheck to paycheck. It means you’ve intentionally directed your money rather than wondering where it went.

Why Traditional Budgeting Often Fails

Most people budget like this:

- Calculate income: $4,000

- Subtract obvious bills: -$2,200

- Assume the remaining $1,800 will “work out”

- Wonder why they can’t save money

The problem? That $1,800 isn’t assigned to anything. It floats around your checking account, slowly leaking into coffee runs, impulse Amazon purchases, and “I deserve this” moments. At month’s end, there’s $47 left, and you have no idea where the rest went.

Zero-based budgeting eliminates the mystery by eliminating unassigned money. When every dollar has a name, it’s much harder for them to wander off.

How to Create a Zero-Based Budget

Calculate Your Income

Start with what you'll actually receive this month after taxes—salary, side hustle income, bonuses, child support. If your income varies, use the lowest reasonable estimate.

List Your Fixed Expenses

These are the non-negotiables: rent/mortgage, car payment, insurance premiums, minimum debt payments, subscriptions, phone/internet. Write down exact amounts—no guessing.

Estimate Your Variable Expenses

These change month to month: groceries, gas/transportation, utilities, personal care, pet expenses. Use last month's spending as a starting point.

Plan Your Savings and Debt Payoff

Savings isn't what's 'left over'—it's a planned expense. Include emergency fund, retirement savings, goal-specific savings, and extra debt payments. Treat savings like a bill.

Budget for Fun (Yes, Really)

A budget that eliminates all enjoyment will fail. Plan for entertainment, dining out, hobbies, and occasional treats. Zero doesn't mean zero fun—it means zero unplanned dollars.

Cover Irregular Expenses

Things that don't happen monthly still need allocation: car repairs, medical expenses, holiday gifts, annual subscriptions. Calculate yearly cost, divide by 12, set aside monthly.

Make It Zero

Add up everything. If you have money left over, assign it somewhere. If you're over your income, cut somewhere—start with wants. The numbers must balance.

Zero-Based Budgeting with Irregular Income

“This sounds great for people with salaries. But I’m a freelancer.”

Good news: zero-based budgeting actually works better for irregular income. Here’s how:

-

Budget with what you have, not what you expect. Only allocate money that’s currently in your account.

-

Prioritize ruthlessly. When income arrives, fund categories in order: essentials first, then savings, then lifestyle.

-

Build a buffer. Your first savings goal should be one month of expenses sitting in your account. This lets you budget a full month ahead instead of scrambling.

-

Expect variability. Some months you’ll fully fund everything. Some months you won’t. That’s okay—the system flexes with you.

Common Zero-Based Budgeting Mistakes

Mistake 1: Forgetting Irregular Expenses

New budgeters often exclude things like car repairs because “that won’t happen this month.” Then it does, and the budget explodes. Always include a monthly allocation for irregular expenses.

Mistake 2: Setting Unrealistic Categories

Budgeting $200/month for groceries when you’ve never spent less than $400 sets you up for failure. Use real numbers from your actual spending, then gradually work toward more frugal targets.

Mistake 3: Not Building in Flexibility

Life happens. Budget a “miscellaneous” or “buffer” category of 5-10% of your income. This handles the unexpected without derailing everything.

Mistake 4: Treating It Like a Set-It-and-Forget-It System

Zero-based budgeting requires monthly attention. Each month is different: holidays, birthdays, seasonal expenses. Budget from scratch each month based on what’s actually happening.

Mistake 5: Giving Up After One Bad Month

You will overspend your budget. Categories will need adjustment. This doesn’t mean the system failed—it means you’re learning. Adjust and continue.

Zero-Based vs. Other Budgeting Methods

| Method | How It Works | Best For | Complexity |

|---|---|---|---|

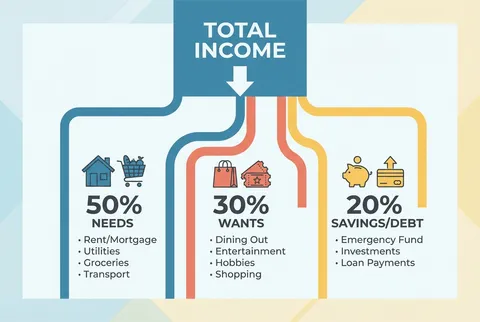

| 50/30/20 | Percentage categories (needs, wants, savings) | Beginners wanting simple guardrails | Low |

| Envelope System | Physical cash in category envelopes | Spenders needing tangible limits | Medium |

| Pay Yourself First | Auto-save, then spend what’s left | Those who struggle with complexity | Low |

| Zero-Based | Every dollar assigned to a specific purpose | People wanting full control and visibility | High |

Many people use hybrid approaches—zero-based planning with 50/30/20 guidelines, for example.

The Real Power of Zero-Based Budgeting

The zero isn’t really about math. It’s about mindset.

When every dollar has a job, you stop making impulse decisions. “Can I afford this?” becomes “What am I willing to take this money from?” The answer is usually “nothing,” and the impulse passes.

Zero-based budgeting creates awareness. You’ll notice patterns—that you spend $200/month on coffee, that entertainment eats 15% of your income, that you’ve been paying for a gym membership you never use. Awareness creates options.

Most importantly, zero-based budgeting puts you in control. You’re not reacting to bank statements in horror. You’re not wondering where the money went. You decided in advance, and now you’re executing the plan.

Your Action Steps This Week

-

Pull your bank statements from the last 3 months. Categorize every expense. This shows your real spending patterns.

-

Calculate your true income for next month. After taxes, after deductions—what actually hits your account?

-

Create your first zero-based budget. Start simple: fixed expenses, variable expenses, savings, fun. Make it balance to zero.

-

Track daily for one month. Every purchase gets logged in BUDGT. No exceptions.

-

Review and adjust. At month’s end, compare planned vs. actual. Learn, adjust, improve.

The Bottom Line

Zero-based budgeting means every dollar has a purpose. Income minus all planned expenses equals zero—not because you’re broke, but because you’ve intentionally directed every dollar.

It takes more effort than vague budgeting. But the payoff is complete clarity about your money. No more wondering where it went. No more month-end surprises. No more hoping savings will happen.

When every dollar has a job, they all show up to work.

Frequently Asked Questions

What is zero-based budgeting in simple terms?

Zero-based budgeting means your income minus your expenses equals zero. Not because you're broke, but because every dollar has an assigned purpose—bills, groceries, savings, investments. When you're done allocating, your 'leftover' is $0 because nothing is left unassigned.

Does zero-based budgeting mean you have zero dollars?

No. A zero-based budget does not mean zero dollars in your account. It means every dollar of your income has been assigned a specific purpose—including savings. If you earn $4,000, you allocate all $4,000 to categories like rent, groceries, savings, and entertainment. The 'zero' refers to unassigned money, not your bank balance.

True or false: A zero-based budget means your income minus expenses equals zero?

True. In a zero-based budget, income minus all planned expenses (including savings and investments) equals exactly zero. This doesn't mean you spend everything—it means every dollar has a job. Savings is treated as an expense category, so money set aside for emergencies or retirement is part of reaching zero.

How does a zero-based budget work?

A zero-based budget works by assigning every dollar of income to a specific category before the month begins. You list all income, then allocate it to expenses, savings, and investments until nothing is left unassigned. Throughout the month, you track spending against each category. If one category runs low, you move money from another.

Should I try a zero-based budget?

Yes, if you want complete control over your money. Zero-based budgeting is ideal for people who want to know exactly where every dollar goes, those paying off debt, or anyone tired of wondering why they can't save. It requires more effort than simpler methods but provides the clearest financial picture.

Is zero-based budgeting the same as starting from zero each month?

Yes! Unlike traditional budgeting where you might adjust last month's numbers, ZBB starts fresh each month. You look at the upcoming month's income and decide from scratch how every dollar will be used. This forces intentional decisions rather than autopilot spending.

Does zero-based budgeting work for irregular income?

Absolutely—it actually works better for irregular income. Instead of guessing, you budget with the money you actually have. When new income arrives, you immediately assign it to categories. This prevents the feast-or-famine cycle many freelancers and commission workers experience.

How is zero-based budgeting different from the 50/30/20 rule?

The 50/30/20 rule gives you percentage guidelines (50% needs, 30% wants, 20% savings) but doesn't track specific dollars. Zero-based budgeting is more detailed—every dollar gets a specific assignment. Many people use 50/30/20 as a framework within their zero-based budget.

What if I have money left over at the end of the month?

In zero-based budgeting, leftover money shouldn't exist—it should already be assigned to savings, investments, or next month's budget. If you consistently have unassigned money, you're either under-budgeting your categories or not planning for irregular expenses like car repairs.

Is zero-based budgeting too time-consuming?

The initial setup takes 1-2 hours. After that, it's 15-30 minutes at month's end to set up the next month, plus a few minutes daily to track spending. Most people find that the financial clarity is worth far more than the time invested.

What categories should I include in a zero-based budget?

Start with essentials: housing, utilities, food, transportation, insurance. Then add lifestyle: entertainment, dining out, subscriptions. Include savings goals: emergency fund, retirement, specific purchases. Finally, don't forget irregular expenses: car maintenance, medical, gifts. The more specific, the better.

Related Articles

Ready to take control of your budget?

Download BUDGT and start tracking your daily spending today.