Budgeting After FIRE: How to Manage Spending in Early Retirement

You’ve done it. Years of aggressive saving, careful investing, and intentional living have paid off. You’ve reached your FIRE number. You’re financially independent.

Now comes the hard part: actually spending the money.

This sounds absurd to anyone still in accumulation mode. “Oh no, I have to spend money, poor me.” But talk to people who’ve achieved FIRE, and you’ll hear the same theme again and again: spending is psychologically harder than saving.

The habits that got you here — the frugality, the delayed gratification, the constant savings rate optimization — don’t automatically reverse when you hit your number. The muscle memory of minimizing expenses remains, even when minimizing is no longer necessary.

Learning to spend your portfolio requires its own transition. And surprisingly, daily budgeting helps with that too.

The Spending Anxiety Problem

For years, maybe decades, you trained yourself to minimize spending. Every purchase was evaluated against your savings rate. Every dollar saved was a step closer to freedom. Spending was the enemy of progress.

That mindset doesn’t vanish when you retire. Many early retirees find themselves:

- Feeling guilty about normal purchases. A $50 dinner feels extravagant even when it’s well within budget.

- Under-spending significantly. Withdrawing 2% when they planned for 4%, missing experiences they could easily afford.

- Constant money anxiety. Checking portfolio balances obsessively, worrying about every market dip.

- Inability to enjoy. Having the financial freedom to travel, dine out, or pursue hobbies, but feeling unable to actually do it.

This is spending anxiety, and it’s remarkably common among FIRE achievers. The same discipline that enabled early retirement now prevents enjoying it.

From Accumulation to Decumulation

The mindset shift required is significant. During accumulation, your goal was to grow your portfolio. Every dollar saved was progress. Spending was literally the opposite of your goal.

In retirement, your portfolio exists to be used. That’s the entire point. You saved this money specifically so you could spend it later. Later is now.

This isn’t permission to be reckless. It’s recognition that chronic under-spending is its own failure mode. If you die with millions unspent, you worked longer than necessary. You saved experiences you could have had. You optimized for a number instead of a life.

The goal isn’t to spend everything. It’s to spend appropriately — enjoying the freedom you’ve earned while ensuring the portfolio lasts.

The 4% Rule in Daily Terms

Abstract annual budgets don’t help with spending anxiety. “I can spend $40,000 this year” doesn’t tell you whether today’s coffee is okay.

Daily budgets make the math tangible:

Your 4% Rule Daily Budget

Enter your numbers above - results update automatically

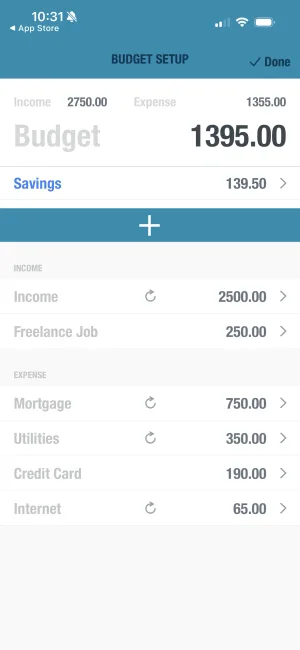

With a $1,000,000 portfolio:

- Annual withdrawal (4%): $40,000

- Monthly: $3,333

- Fixed expenses: $1,500

- Available: $1,833

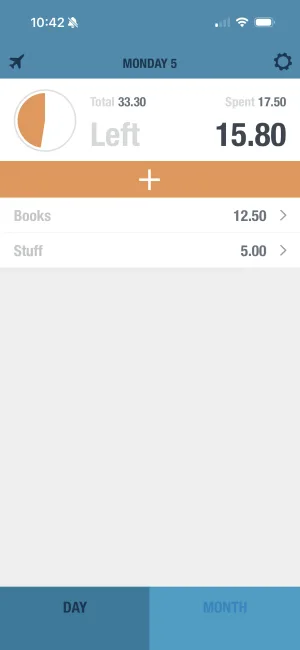

- Daily budget: $61

That $50 dinner? It’s less than one day’s budget. That $15 coffee? It’s a quarter of what you can spend today. Suddenly, these purchases fit clearly within what the math supports.

Why Daily Visibility Helps Spending Anxiety

Spending anxiety comes from uncertainty. “Am I spending too much? Will I run out? Is this purchase okay?” Without clear feedback, every purchase triggers doubt.

Daily budgeting provides constant reassurance:

Real-time permission. Your daily budget tells you exactly what you can spend today. Under it? You’re fine. No guilt needed.

Accumulated buffer. When you underspend (which anxious retirees often do), the surplus accumulates. That growing buffer provides psychological cushion for larger purchases.

Visible sustainability. Staying under your daily limit day after day proves the system works. Your portfolio can sustain this. The math is visible, not abstract.

Natural adjustments. Spend more one day, less the next. The system self-corrects without requiring conscious restriction. Flexibility without anxiety.

Variable Spending in Retirement

Retirement spending isn’t constant. Some months feature travel, home projects, or family visits. Others are quiet months at home. A rigid monthly budget doesn’t fit this reality.

The daily budget method handles variability naturally:

Month overflow. Underspend in January (quiet month at home), and that surplus carries into February. When you take that trip in March, you have accumulated buffer to draw from.

No category guilt. Travel doesn’t compete with dining or entertainment for envelope allocation. It all comes from the same daily budget pool. Spend more on travel this month, less on dining. The categories don’t matter — total daily spending does.

Annual perspective. Some months over, some months under. What matters is the annual picture. Daily tracking keeps you aware without requiring each month to balance perfectly.

Sequence of Returns Awareness

Early retirement introduces sequence of returns risk: poor market performance in early retirement years hurts more than later. A 30% drop when you’re 35 and still contributing is a buying opportunity. The same drop when you’re 45 and withdrawing is a threat.

Daily budget tracking creates natural awareness of this risk without panic:

Visible portfolio connection. When markets drop, your daily budget reflects it (if you recalculate based on current portfolio value). You naturally spend less because your budget shows less.

Gradual adjustment. Small daily reductions are psychologically easier than dramatic lifestyle cuts. Spending $50/day instead of $60/day feels like minor adjustment, not deprivation.

No panic required. You don’t need to make big decisions in the moment. Just follow your daily budget, which already reflects the changed reality. The system adapts without emotional reactions.

This is the “guardrails” approach to retirement spending: naturally spending less when portfolio is down, more when it’s up. Daily budgeting makes this intuitive rather than requiring conscious strategy.

Travel Mode for the Early Retiree

Extended travel is a common early retirement dream. Different cities, different countries, different costs. Budgeting while traveling presents unique challenges.

Travel mode solves this:

Separate travel budget. Set a different daily limit for travel that reflects trip costs. $100/day in Southeast Asia, $200/day in Western Europe, whatever matches your travel style.

Currency flexibility. Track in local currency without conversion confusion. You know what the local amount means against your local daily limit.

Offline functionality. Log expenses anywhere — no WiFi, no roaming charges, no worrying about connectivity in remote locations.

The Post-FIRE Daily Budget Setup

Setting up your retirement daily budget takes just a few minutes:

Step 1: Know your portfolio. Total invested assets across all accounts.

Step 2: Choose your withdrawal rate. 4% is traditional. 3.5% is conservative. 4.5% if you have other income sources or shorter time horizon.

Step 3: Calculate monthly withdrawal. (Portfolio × withdrawal rate) ÷ 12

Step 4: Subtract fixed expenses. Housing, utilities, insurance, healthcare, subscriptions. Everything that doesn’t vary.

Step 5: Divide by days. What’s left divided by 30 (or exact days in month) is your daily budget.

Step 6: Track daily. Log expenses as they happen. Check your status before purchases. Adjust naturally.

Permission to Spend

Here’s what took me years to internalize after reaching FIRE:

Your portfolio is meant to be used. You didn’t save this money to look at a number. You saved it to fund a life.

Under-spending is not a virtue. Dying with millions is not a success story. It’s years of extra work for money you never used.

Experiences have value. That trip you’re hesitating on? That dinner with friends? That hobby equipment? These are what the portfolio is for.

Daily budgets provide guardrails. You’re not spending blindly. You know exactly what’s sustainable. Stay under your daily limit, and you can spend without guilt.

The discipline that got you to FIRE was valuable. It enabled this freedom. But now that discipline must evolve. The goal isn’t maximum frugality anymore. It’s appropriate spending — enjoying the freedom you’ve earned while ensuring sustainability.

Your daily budget gives you permission. If you’re under it, spend freely. You’ve done the math. You’ve built the portfolio. This is what it’s for.

The Retirement You Earned

Financial independence isn’t just about reaching a number. It’s about the life that number enables. The freedom to spend your days as you choose. The ability to say yes to experiences without financial stress.

But freedom requires comfort with spending. Without that, you’ve achieved financial independence but not the psychological independence to enjoy it.

Daily budgeting bridges this gap. It provides the certainty that anxious retirees need: visible proof that spending is sustainable. Real-time feedback that each purchase is okay. Mathematical reassurance that the portfolio can handle this lifestyle.

You’ve earned this retirement. Daily awareness helps you actually enjoy it.

Frequently Asked Questions

Why is spending harder than saving after FIRE?

Years of aggressive saving build strong frugal habits and spending anxiety. The mindset that got you to FIRE — minimize expenses, maximize savings — doesn't automatically reverse when you reach your number.

How do I know if I'm spending too much in early retirement?

Track your daily spending against your 4% rule limit. If you're consistently under your daily budget, you're fine. Most early retirees under-spend out of anxiety, not over-spend from carelessness.

Should I adjust spending when markets drop?

Flexible withdrawal strategies work well — spending slightly less in down years, more in up years. Daily budget tracking makes these adjustments feel natural rather than panicked.

What's a realistic daily budget in early retirement?

It depends on your portfolio and fixed expenses. With a $1M portfolio and $1,500 monthly fixed costs, you'd have about $60/day for discretionary spending using the 4% rule.

How do I handle variable spending in retirement?

Some months you'll travel, others you'll stay home. Month overflow carries unused budget forward, letting you flex spending while staying on track annually.

Related Articles

Ready to take control of your budget?

Download BUDGT and start tracking your daily spending today.