Why I Track Spending Without Connecting My Bank Accounts

When I tell people I track every expense manually instead of using auto-sync, they look at me like I’m using a flip phone by choice.

“Why would you do that? Mint does it automatically.”

Here’s the thing: I used auto-sync apps for years. They were convenient. They were also why I never really changed my spending behavior. The transactions just… appeared. I’d scroll through them, maybe categorize a few, and close the app feeling vaguely informed but not actually different.

Manual tracking changed that. Every expense I log is a conscious decision. A micro-moment of reflection. “Do I really need to record another coffee shop visit this week?” That friction — the same friction that makes auto-sync feel superior — is actually the feature.

But there’s another reason I went manual, one that matters more as my portfolio grows: privacy.

The Convenience Trap

Auto-sync budgeting apps make a compelling promise: connect your accounts once, and we’ll do the rest. No logging, no categorizing, no effort. Just insights.

What they don’t emphasize: they’re accessing your complete financial picture. Every transaction. Every balance. Every account. And they’re storing it on their servers.

Services like Plaid (which powers most auto-sync features) require your bank login credentials. They access your accounts using the same permissions you have — meaning they can see everything. Transaction history. Account balances. Connected accounts. Recurring payments.

For most people, this feels like an acceptable trade-off. Convenience for data access. But for those pursuing FIRE — often with six or seven figures in invested assets — the calculus changes.

The Privacy Calculation

I’m not suggesting auto-sync apps are malicious. Most are well-intentioned companies trying to help people budget better.

But consider:

- Data breaches happen. Financial technology companies have been breached. Your transaction history is valuable data for identity thieves, marketers, and anyone trying to profile your financial life.

- Business models matter. Free apps need revenue. If you’re not paying, your data is often the product — sold to marketers, used for targeting, or monetized in ways you didn’t anticipate.

- Access creep. What starts as transaction access can expand. Terms of service change. Companies get acquired. Data that seemed harmless becomes part of a larger profile.

The FIRE community is particularly privacy-conscious for good reason. We often have significant assets, unusual spending patterns (low relative to income), and a desire to fly under the radar. Giving a third party visibility into all of that feels like unnecessary exposure.

The Awareness Argument

Privacy aside, there’s a practical reason to track manually: it works better.

The friction of logging expenses isn’t a bug — it’s the feature. When you have to type in “$4.50 - coffee,” you’re forced to acknowledge that purchase. When it auto-imports as one of 47 transactions you scroll past, it disappears into the noise.

This isn’t just my opinion. Research on spending awareness consistently shows that active engagement with expenses changes behavior more than passive observation. The same reason cash feels more “real” than credit cards applies to manual versus automatic tracking.

Every manual entry is a micro-decision: “Was this purchase worth recording? Was it aligned with my goals?” Those questions don’t arise when transactions just appear.

What You Gain vs What You Lose

Let’s be honest about the trade-offs:

What you lose:

- Auto-import (saves maybe 5 minutes per week)

- Automatic categorization (though it’s often wrong anyway)

- Historical import (can’t see transactions before you started tracking)

What you gain:

- Complete privacy. Your financial data never leaves your device. No server. No cloud. No third party.

- Spending awareness. Active logging creates mindfulness that passive importing can’t match.

- No account required. No username, no password, no email harvesting.

- Offline functionality. Works anywhere — no internet required.

- No dependency. If the app company shuts down, your data is still yours.

- Security. Can’t breach what isn’t on a server.

For most FIRE folks I know, the trade-off is obvious. Five minutes of logging per week versus complete visibility into your financial life? The math isn’t close.

The 30-Second Habit

Manual tracking sounds tedious until you actually do it. Here’s what it looks like in practice:

- Buy something. Coffee, groceries, gas, whatever.

- Open app. Takes 2 seconds.

- Log expense. Amount, category, optional note. Takes 10-15 seconds.

- Done. Close app.

Total time per expense: about 30 seconds.

Most people make 3-5 purchases per day. That’s 2-3 minutes of logging. For that minimal investment, you get real-time awareness of your daily spending and complete control over your financial privacy.

The habit forms quickly. Within a week or two, logging feels automatic — like locking your car or checking your phone. You don’t think about it; you just do it.

Making Manual Entry Stick

The key to sustainable manual tracking: make it frictionless.

Log immediately. Don’t wait until end of day to remember what you spent. Log when you spend. The expense is fresh, and you won’t forget anything.

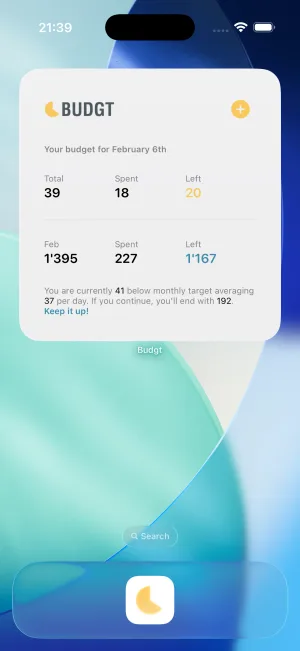

Use a widget. BUDGT’s home screen widget lets you log expenses without even opening the app. Tap, enter amount, done.

Keep categories simple. You don’t need 47 categories. 5-10 broad categories that match how you think about spending work better than granular complexity.

Don’t stress perfection. Forgot to log lunch? Add it when you remember. Missed a small expense? Not worth stressing over. The goal is awareness over time, not forensic accuracy.

Review weekly. Spend 5 minutes weekly reviewing what you logged. Patterns become obvious. No auto-generated report needed.

The Minimalist Approach

There’s something philosophically aligned between manual tracking and the FIRE mindset.

FIRE is about intentionality. Spending money deliberately, not by default. Choosing what you value over what’s marketed to you. Taking control instead of being controlled.

Manual expense tracking is the same philosophy applied to financial tools. Instead of surrendering your data to an algorithm that tells you what to think about your spending, you engage directly. You decide what matters. You build awareness through action, not passive observation.

It’s slower. It’s less automated. It’s also more yours.

Privacy in an Exposed World

We leak data constantly. Social media tracks our interests. Phones track our location. Credit cards track our purchases. Most of this is unavoidable without significant lifestyle changes.

Financial data is different. It’s one of the few areas where you can make a complete choice. You can choose to share your transaction history with Plaid, Mint, YNAB, or any number of services that want visibility into your money.

Or you can keep it entirely private. Log expenses yourself. Store data on your device only. Never connect to a server.

For those of us building wealth toward financial independence, the latter feels right. We’re already going against the grain — saving half our income, planning to retire decades early, questioning consumer culture. Keeping our financial data private is just one more way of maintaining control.

Your Data, Your Choice

I’m not here to tell you auto-sync is evil. For many people, the convenience genuinely helps them start budgeting when they otherwise wouldn’t. Any budgeting is better than no budgeting.

But if you’re privacy-conscious — and especially if you’re building significant wealth — it’s worth questioning whether convenience is worth the trade-off.

You can track every expense while sharing nothing with anyone. Your financial life can be completely private. The only cost is 2-3 minutes per day of intentional logging.

For me, that’s not a cost. It’s the point.

Frequently Asked Questions

Why would I track expenses manually when auto-sync exists?

Manual entry creates awareness that auto-sync removes. Every expense logged is a moment of reflection. Studies show that friction in spending creates mindfulness — you think twice about purchases when you have to record them yourself.

Is it safe to connect my bank to budgeting apps?

It depends on your risk tolerance. Services like Plaid access your full transaction history and balances. While they use encryption, data breaches in fintech have occurred. For those with significant assets (common in FIRE), the privacy risk may outweigh the convenience.

How much time does manual expense tracking take?

About 30 seconds per expense, or 5-10 minutes daily for most people. Many find this pays for itself in reduced impulse spending — the act of logging creates a natural pause before purchases.

What if I forget to log an expense?

Check your bank statement weekly for anything you missed. Most people develop the habit within 2-3 weeks, especially when using a widget for quick entry. The occasional missed expense matters less than the overall awareness you build.

Can I still track spending while traveling without internet?

With an offline app like BUDGT, yes. Your data stays on your device and syncs nothing to the cloud. Log expenses anywhere — no WiFi, no roaming charges, no worrying about security on public networks.

Related Articles

Ready to take control of your budget?

Download BUDGT and start tracking your daily spending today.