End-of-Month Budget Review: Your 5-Minute Checklist

The month is ending. Your budget app has 30 days of data. Now what?

Most people either ignore their budget entirely or spend hours obsessing over every transaction. There’s a better way: a quick, focused review that takes 5 minutes and actually improves next month.

Why Monthly Reviews Matter

Daily tracking keeps you aware. But monthly reviews reveal patterns you can’t see day-to-day:

| Daily View | Monthly View |

|---|---|

| ”I spent $45 today" | "I spend $180/week on food" |

| "I’m over budget today" | "I overspend every Friday" |

| "Random coffee purchase" | "Coffee adds up to $120/month” |

The monthly review connects dots. It’s where insights happen.

The 5-Minute End-of-Month Checklist

Check your bottom line (1 min)

Did you spend more or less than your budget allowed? Just the big picture number.

Spot the top 3 categories (1 min)

Where did most of your money go? Any surprises?

Find the outliers (1 min)

Any unusually large expenses? Were they planned or impulse?

Check your savings (1 min)

Did you hit your savings goal? If not, how close?

Set one intention for next month (1 min)

One thing to do differently. Just one.

That’s it. Five minutes, five questions, done.

Step 1: Check Your Bottom Line

Open your budget app. Look at the month summary.

| Question | What It Tells You |

|---|---|

| Did I stay under budget? | Basic success metric |

| By how much (over or under)? | Margin for error or room to save more |

| How does this compare to last month? | Trend direction |

Don’t overthink this step. You just want to know: good month, bad month, or somewhere in between?

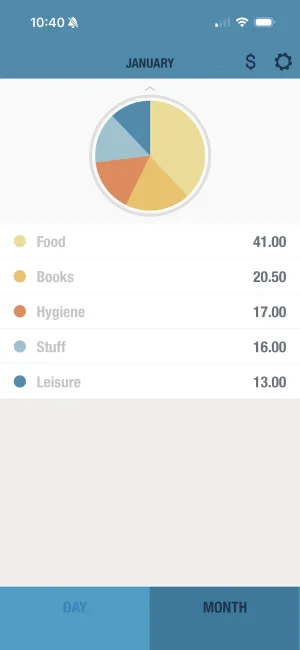

Step 2: Spot Your Top 3 Categories

Where did the money actually go?

| Category | This Month | % of Total |

|---|---|---|

| #1 | $ | % |

| #2 | $ | % |

| #3 | $ | % |

Most people find their top 3 categories account for 60-70% of all spending. These are your leverage points — small improvements here have the biggest impact.

Questions to ask:

- Are these the categories I want to prioritize?

- Any category surprisingly high?

- Any category I thought would be higher?

Step 3: Find the Outliers

Look for transactions that stand out:

| Outlier Type | Example | What to Do |

|---|---|---|

| Planned large expense | Car repair, medical bill | Expected — no action needed |

| Unplanned large expense | Emergency, impulse buy | Note it — was it avoidable? |

| Recurring surprise | Subscription you forgot | Cancel or budget for it |

| Unusual pattern | 5 Amazon orders in one week | Investigate the trigger |

Outliers aren’t automatically bad. But they should be intentional.

Step 4: Check Your Savings

Did you hit your savings target?

| Savings Goal | Actual | Status |

|---|---|---|

| $ | $ | ✓ or ✗ |

If you missed it:

- By a little — Normal variance, stay the course

- By a lot — Something needs to change (income, spending, or goal)

- Didn’t save at all — Red flag, investigate why

If you exceeded it:

- Great! Consider increasing next month’s goal

- Or keep the buffer for irregular months

Step 5: Set One Intention

Not ten goals. Not a complete budget overhaul. One thing.

| Pattern You Noticed | One Intention |

|---|---|

| Overspent on dining | Pack lunch 3x this week |

| Too many small Amazon purchases | Implement 24-hour rule |

| Forgot about annual subscription | Add it to next month’s budget |

| Crushed your savings goal | Increase savings by $50 |

One focused change is achievable. Ten changes means nothing changes.

The Review Template

Copy this for your monthly review:

MONTH: ____________

1. BOTTOM LINE

Budget: $______ Actual: $______ Difference: $______

2. TOP 3 CATEGORIES

1. _____________ : $______

2. _____________ : $______

3. _____________ : $______

3. OUTLIERS

-

-

4. SAVINGS

Goal: $______ Actual: $______ Hit target? Y/N

5. ONE INTENTION FOR NEXT MONTH

_________________________________Common Review Mistakes

Mistake 1: Getting Too Detailed

You don’t need to analyze every $3 transaction. Focus on patterns, not pennies.

| Too Detailed | Just Right |

|---|---|

| ”Why did I spend $3.47 at CVS on the 14th?" | "I spent $45 at drugstores this month — more than usual” |

| Categorizing every receipt | Knowing your top 3-5 categories |

| Matching bank statement to the penny | Trusting your tracking was consistent |

Mistake 2: Only Looking at Negatives

Celebrate wins too:

| Win | Why It Matters |

|---|---|

| Stayed under budget | Proves it’s possible |

| Saved more than planned | Momentum builder |

| No impulse purchases | Pattern is changing |

| Caught a subscription you forgot | Saved future money |

Mistake 3: Making Too Many Changes

One month of data isn’t enough to overhaul your entire budget.

| After One Month | After Three Months |

|---|---|

| Note the pattern | Confirm the pattern |

| Make one small adjustment | Consider bigger changes |

| Keep tracking | Adjust budget categories |

When to Do a Deeper Review

The 5-minute checklist works for normal months. Do a longer review (15-30 minutes) when:

| Situation | What to Review |

|---|---|

| Income changed | Recalculate daily budget from scratch |

| Big life event | New expense categories, adjusted priorities |

| Consistently over budget | Where the system is breaking down |

| Every quarter | Overall trends and goal progress |

Building the Habit

The best review is the one you actually do. Here’s how to make it stick:

| Strategy | How It Helps |

|---|---|

| Same day each month | Becomes automatic (1st or last day works) |

| Pair with existing habit | ”After I pay rent, I review budget” |

| Keep it short | 5 minutes is doable; 30 minutes gets skipped |

| Use the same template | No decision fatigue about what to look at |

The Bottom Line

A monthly budget review doesn’t need to be complicated:

- Check your bottom line — Over or under?

- Spot top categories — Where did money go?

- Find outliers — Anything unusual?

- Check savings — Did you hit your goal?

- Set one intention — One thing to improve

Five minutes. Five questions. Every month.

The goal isn’t perfection — it’s awareness. And awareness, consistently applied, leads to better decisions.

Ready for your monthly review? BUDGT shows your month summary, category breakdown, and trends — everything you need for a quick check-in.

Frequently Asked Questions

How often should I review my budget?

At minimum, do a thorough review once a month. Many people find a quick daily check (30 seconds) plus a weekly glance (2 minutes) keeps them on track, with the monthly review being the deep dive.

What should I look for in a monthly budget review?

Focus on: Did you stay within your daily budget most days? Which categories had the most spending? Were there any surprise expenses? Did you hit your savings goal? What patterns do you see?

How long should a budget review take?

A basic monthly review can take as little as 5 minutes if you've been tracking consistently. If you need to categorize transactions or reconcile accounts, allow 15-30 minutes.

What do I do if I went over budget?

Don't panic. Identify why (one-time expense vs. pattern), adjust next month's expectations if needed, and move forward. The goal is awareness, not perfection. Every month is a fresh start.

Should I adjust my budget every month?

Only if something significant changed (income, new expense, goal shift). Frequent adjustments can mask overspending patterns. Give your budget 2-3 months before major changes.

Related Articles

Ready to take control of your budget?

Download BUDGT and start tracking your daily spending today.