Frugal Living at 60: Smart Money Habits for a Comfortable Retirement

By the time you reach 60, you’ve likely forgotten more about stretching a dollar than most budgeting blogs will ever teach. You’ve raised families, weathered recessions, and learned the difference between what’s worth spending on and what isn’t. Frugal living at this stage isn’t about learning to cut back — it’s about applying a lifetime of good judgment to a new chapter, often on a more fixed income.

The goal here is simple: make your money go comfortably further, without giving up the things that make life good. No deprivation, no lectures — just practical habits and tools that respect both your intelligence and your privacy.

Why Frugal Living Is Different at 60

Your 60s bring a genuine shift. Income often becomes fixed — a pension, Social Security, retirement withdrawals — so the game changes from “earn more” to “make what I have last.” The good news: you also have advantages you didn’t at 30.

| What changes at 60 | Why it helps |

|---|---|

| Income is more fixed | Predictable — you can plan precisely around a known number |

| More time | Time to cook, compare prices, and do things yourself |

| Decades of experience | You already know your real needs from passing wants |

| Fewer dependents | Often lower baseline expenses than in your 40s |

| Eligible for senior discounts | Real savings on travel, dining, groceries, and more |

Frugality at 60 isn’t a step down. Handled well, it’s what buys you the freedom to enjoy this chapter without money worry humming in the background.

Know Your One Number

Everything starts with a single figure: what you can comfortably spend each day after your fixed costs and any savings are set aside. It sounds basic, but knowing it — and glancing at it — is what keeps a fixed income from quietly slipping away.

Add up your monthly income

Pension, Social Security, annuity, and any retirement withdrawals — your reliable monthly total.

Subtract your fixed costs

Housing, utilities, insurance, phone, and any subscriptions you keep.

Set aside anything for savings or gifts

Even in retirement, many like to keep building a little or set money aside for family.

Divide what's left by the days in the month

That's your daily spending limit for groceries, outings, and everyday life.

Frugal Habits That Actually Move the Needle

You don’t need a hundred tips. A handful of consistent habits do most of the work:

| Habit | Why it pays off |

|---|---|

| Review recurring bills yearly | Insurance, phone, and utility providers count on you not checking — a few calls can save hundreds |

| Cook at home, plan around sales | The single biggest lever on a grocery budget |

| Ask for the senior discount | Many go unadvertised — always ask; it adds up |

| Right-size housing and transport | The two largest costs; even small reductions free up real money |

| Shop off-peak and secondhand | Quality items at a fraction of the price, with time to hunt for them |

| Track what you spend | Nothing slips away unnoticed when you can see it |

Frugal, Not Cheap

There’s an important distinction. Frugal isn’t about always buying the cheapest option — it’s about spending deliberately. Pay happily for the good coffee, the trip to see the grandchildren, the tool that lasts. Cut ruthlessly on the things you won’t miss. That’s how frugality feels like freedom instead of sacrifice.

Making a Fixed Income Stretch

When income is fixed, the wins come from two places: lowering your fixed costs and spending your flexible money intentionally.

Lower the fixed costs once, benefit all year:

- Call your insurers and providers annually — loyalty rarely pays; asking does.

- Reassess whether your home and vehicle still fit your life. Downsizing either can transform a budget.

- Prune subscriptions to the few you genuinely use.

Spend the flexible money on purpose:

- Use your daily number as a gentle guide, not a cage.

- Batch errands and plan around sales and discount days.

- Favor experiences and time with people over things — they’re often cheaper and always more valuable.

A Note on Privacy and Simple Tools

A lot of budgeting apps want to connect directly to your bank accounts. That’s a reasonable thing to be wary of — the fewer places holding your banking login, the better. You shouldn’t have to trade your privacy for a clear budget.

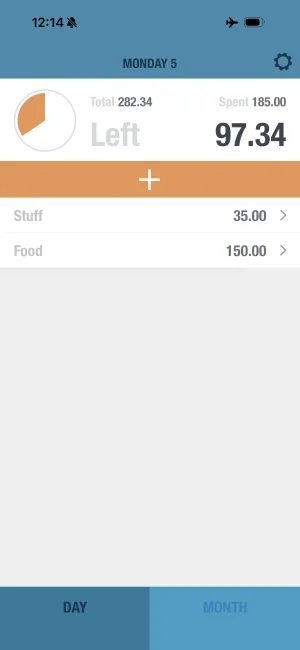

That’s exactly why BUDGT works the way it does: no bank connection, everything stored on your own device, and full offline functionality. You enter your numbers, you see your daily limit, and your financial life stays private. It’s a modern tool that respects an old-fashioned value — minding your own business.

The Once-a-Year Bill Review That Pays for Itself

If you do only one thing from this guide, make it this: once a year, sit down and review every recurring bill you have. Providers count on inertia — they quietly raise prices knowing most people won’t check, and loyalty is routinely punished rather than rewarded. An hour of phone calls can be the best-paid hour of your year.

Work through them one at a time:

- Insurance (home, auto, and supplemental): Get fresh quotes from competitors, then call your current provider and ask them to match or beat. Bundling policies often unlocks a discount, and your rate should reflect that you’re a lower-risk driver than you were decades ago.

- Phone and internet: These are the worst offenders for creeping prices. Call, mention you’re reviewing your budget, and ask what promotions are available — there’s almost always a cheaper plan they didn’t volunteer. Retention departments exist precisely to keep you.

- Streaming and subscriptions: Look at everything billing you monthly and be honest about what you actually use. Keep the few you love, cancel the rest, and remember you can always resubscribe.

- Medications: Ask your pharmacist about generics and discount programs, and compare prices between pharmacies — they vary more than most people expect.

The beauty of this habit is that each win keeps paying all year long. Trim $40 a month across a few bills and that’s nearly $500 back in your pocket over the year, for one afternoon’s effort.

Senior Discounts Worth Asking About

One of the genuine perks of this stage is that a lot of the world quietly offers you a better price — if you ask. Many senior discounts are unadvertised, and the eligibility age is often lower than people assume (sometimes 55, frequently 60 or 62). It never hurts to ask a simple “do you offer a senior discount?” — the worst case is a polite no.

The categories where it adds up most: groceries (many stores run a senior discount day), pharmacies, restaurants, travel and hotels, public transit and rail, museums and cinemas, and even some phone and insurance plans. None of these is life-changing on its own, but as a habit — asking, every time — they compound into real money over a year, on things you were buying anyway.

Should You Downsize?

Housing is almost always the largest line in a budget, which makes it the biggest lever you have. For many people in their 60s, the family home is larger and more expensive to run than their current life actually needs — and right-sizing it can transform the math.

Downsizing isn’t only about a smaller mortgage or none at all. A smaller or newer home usually means lower utility bills, less maintenance, lower property taxes and insurance, and often the release of significant equity that can bolster your retirement savings. It can also simply mean less to clean and worry about — a lifestyle win as much as a financial one.

It’s a big, personal decision and not the right move for everyone; there are real emotional and transactional costs to weigh. But it deserves an honest look rather than an automatic “we’ll stay put.” Even downsizing one vehicle, or renting out a spare room, can free up meaningful monthly money without moving at all. The question worth asking is simply: does what I’m paying to house myself still fit the life I’m actually living?

The Bottom Line

Frugal living at 60 is simply good judgment applied to a new season. Know your one daily number, keep your fixed costs lean, spend deliberately on what you value, and use tools simple and private enough to actually fit your life. Do that, and a fixed income doesn’t feel like a limit — it feels like enough, with room to enjoy the years you worked so hard for.

You’ve earned the freedom that careful money habits bring. This is just about keeping it.

Frugal living is easier with one clear number. BUDGT shows your daily spending limit — no bank connection, fully offline, entirely private — so making your money last stays simple and yours.

Frequently Asked Questions

What does frugal living at 60 actually mean?

It means being intentional with money so a fixed or reduced income stretches comfortably — spending deliberately on what matters to you and trimming what doesn't. It's a skill built over a lifetime, not deprivation. Done well, frugal living in your 60s buys freedom and peace of mind, not a smaller life.

How can I live frugally on a fixed income?

Start by knowing your monthly number: total income minus fixed costs equals what's left for everyday spending. From there, review recurring bills once a year (insurance, phone, utilities, subscriptions), cook more meals at home, use senior discounts, and give every remaining dollar a purpose. A simple daily spending limit keeps you comfortably inside your means.

What are the best frugal habits for people over 60?

The highest-impact habits are: reviewing and negotiating recurring bills annually, right-sizing housing and transport, planning meals around sales, using senior and off-peak discounts, and tracking spending so nothing slips through unnoticed. Small consistent habits matter far more than dramatic cuts.

Do I need to connect my bank to a budgeting app?

No — and many people in their 60s prefer not to. Apps that require bank connections raise real privacy and security concerns. BUDGT works with no bank connection at all: you enter your income and expenses yourself, everything stays on your device, and it works fully offline. You get the clarity without handing over your bank login.

How much should I have saved by 60?

A common guideline is roughly 6–8 times your annual income saved by age 60, but the honest answer depends on your expenses, health, and plans. Rather than chase a single number, focus on what you can control: keeping fixed costs low, spending intentionally, and making your savings last. Frugal habits meaningfully extend how far what you have will go.

Is frugal living the same as being cheap?

No. Being cheap means always choosing the lowest price. Frugal means spending deliberately — happily paying for quality and experiences that matter to you, while refusing to waste money on things that don't. It's about value and intention, not just cost.

Related Articles

Ready to take control of your budget?

Download BUDGT and start tracking your daily spending today.